[ad_1]

The oft forecasted Recession hasn’t but appeared. Has it been prevented (i.e., “soft-landing”)? A have a look at the rising proof leads us to conclude that the Recession is coming; we suspect that when the NBER will get round to relationship it, this quarter (This autumn) will mark its starting.

Earnings Expectation Adjustments in This autumn

The primary proof of this confirmed up within the current employment knowledge. And customers (2/3rds of GDP) are simply beginning to alter after a spending spree with the “free cash” doled out by Uncle Sam in 2021 and 2022. Bank card balances are actually at file ranges (and at rates of interest within the mid-20% vary). Delinquencies are actually rising. Earnings expectations for the Retail trade are being minimize as main retailers scale back steering. And inventory analysts have been chopping their earnings forecasts (see chart). Banks have in the reduction of on employees and have restricted lending each to customers and companies whereas upping their mortgage loss reserves. Housing affordability is at a 35-year low due to excessive costs, however equally guilty are mortgage charges, now at 8%. As for inflation, that’s about the one excellent news; it seems to be like it’s melting.

Employment

October was the primary month shortly to point out employment weak spot. As famous in our final weblog, when the revisions (-101K) and Delivery/Dying mannequin add-on (+127K) are accounted for, the payrolls had been really unfavorable within the Institution Survey. The Family Survey, which wasn’t talked about wherever within the media, registered -348K internet jobs. And if it weren’t for the autumn within the Labor Power Participation Price (discouraged candidates), the U3 Unemployment Price would have risen greater than the +0.1 proportion level that introduced it to three.9% (the low was 3.4% final December). Be that as it might, within the post-WWII period, an increase of 0.5 proportion factors in U3 has signaled a Recession 100% of the time. So, those who imagine within the “soft-landing” state of affairs should additionally imagine that “this time is completely different.” (As Warren Buffet famously mentioned: “What we be taught from historical past is that individuals don’t be taught from historical past.”)

In line with Rosenberg Analysis, over the previous three months, the Family Survey has proven a -40K decline in job holders and +665K extra unemployed folks. To indicate the stress on family budgets, over these three months, the variety of a number of job holders has risen by +243K to a close to file 8.4 million.

A number of Jobholders: each first and second jobs are full-time

Within the newest Challenger survey, layoffs had been up 8% from a yr in the past in October, and hiring bulletins had been down -85%. Retail’s seasonal hiring is the bottom since 2008; that claims one thing about what retailers consider upcoming vacation gross sales. As well as, the U6 unemployment price, a extra complete view of the employment image, additionally rose, however by 0.2 proportion factors to 7.2% (this was at a low of 6.5% final December). We additionally word that the variety of corporations asserting massive layoffs is rising with a number of new bulletins every week.

Whereas the employment image has moved towards “stability” from the place it was in 2022 and early 2023, we anticipate that it’ll transfer handed “balanced” and deteriorate. The character of the cycle is that it all the time goes by means of “impartial” or “balanced,” each when it rises AND when it falls. October often is the first of many such weak employment reviews.

One other indicator of job weak spot is employment within the head-hunting enterprise. It has contracted, down -115K since February. When the head-hunting enterprise is struggling, it’s a signal of a weak job market.

illustration of roles in layoffs

Customers

One of many causes that the U.S. financial system has remained in development mode is the “resilient” shopper. Sadly, that seems to be altering. As famous above, the “free cash” from Uncle Sam saved the buyer buoyant, not less than by means of Q3. Now there’s purpose to imagine that the “free cash” has been spent.

“Extra Financial savings” Impression is Over

The chart exhibits the financial savings price for the reason that flip of the century. Notice that financial savings have fallen almost to their 2008 stage and that the majority of that “free cash” has been spent. There seems to be no reservoir or reserve.

Notice additionally that bank card balances are at file ranges, $1.1 trillion, up 16% yr over yr. The chart exhibits that bank card debt now totals $3,800 per capita, up $1,000 per individual since October 2021.

Credit score Card Debt Steadiness Per Capita

Most American households pay for day-to-day gadgets (groceries, gasoline) with a bank card. So, as costs have risen, so have card balances. Delinquencies have risen too, now at 5.8% (up 0.7 proportion factors in Q3). Auto delinquencies have risen in tandem with bank cards, now at 7.4% of excellent balances in Q3. And a couple of.5% are over 90 days overdue, retaining the repo man busy!

Credit score Card Delinquencies & Auto Mortgage Delinquencies 90+ Days

Nowhere is the inflation chew extra evident than within the rate of interest on these bank cards. All of them are 20%+ and a few strategy 30%. For the low- and middle-income households, it has develop into more and more laborious to maintain up. Many have maxed their bank card limits. Sadly, the banks have been denying requests for elevated limits (and requests for brand spanking new playing cards) at near-record or file ranges. Extra cardholders are being charged late charges, are falling behind on minimal funds, and are going through increased prices on a rising debt burden. About 10% of card customers had been in “persistent debt,” a time period used when cardholders pay extra in curiosity and charges every year than what they pay towards the principal.

New Card and Request for Restrict Improve Rejection Charges

Now that the “free cash” has been spent and there’s little room left on the bank card line, there’s nothing left to do however in the reduction of. The fact is that even modest cutbacks, if widespread, have vital financial penalties, together with Recession.

We word that auto gross sales fell in October (-1.2% from September). They’re now down in three of the final 4 months. And the most recent Fed Senior Mortgage Officer Opinion Survey (SLOOS) signifies that banks have continued to tighten lending requirements in This autumn, and that features for autos.

The Enterprise Sector

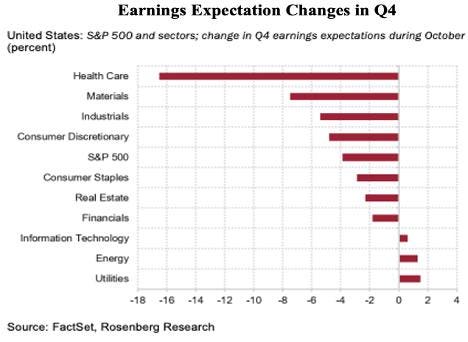

The financial system can’t be excellent when earnings expectations in seven out of 10 sectors are falling. The chart exhibits that well being care prices prepared the ground with a -16%+ discount in This autumn earnings. For the S&P 500 as a complete, expectations are for a -4% in earnings development. The fairness market is kind of delicate to those earnings’ expectation adjustments.

Earnings Expectation Adjustments in This autumn

As well as, we see that Johnson Redbook reported a -1.5% fall in similar retailer gross sales in October and the large field shops like Goal

TGT

WMT

Now we have famous in previous blogs that Manufacturing is already in Recession. The ISM Manufacturing PMI at 46.7 for October has been in contraction (under 50) for 11 months in a row.

ISM Manufacturing PMI

And the ISM Companies PMI was 51.8 in October, down from 53.6 in September and disillusioned the consensus forecast of 53.0. It, too, seems to be headed for contraction, and shortly.

Banking

As a result of credit score is the lifeblood of the financial system, when the banking sector contracts, the financial system fades. And banks are contracting. Because the March Regional Financial institution blow-up, banks have:

- Misplaced deposits;

- Decreased lending in each mortgage sort, and are denying purposes for a rise in bank card traces on the highest price in historical past. As well as, they’ve additionally tightened mortgage lending requirements;

Banks Tightening Credit score to Giant and Small Companies

- Have rising delinquencies in shopper, auto, and business mortgage sectors;

- Are all elevating their mortgage loss reserves;

- New shopper loans, auto loans, and bank card loans are at or close to historic lows;

- Within the Regional Banking area, Business Actual Property (CRE) mortgage points are rising. 15 of 18 Regional Banks reported growing charge-offs and people non-performing loans had risen 80% from Q3 ’22.

Housing

The Housing Trade continues to slip as mortgage charges strategy 8%. Affordability is at its lowest stage for the reason that Eighties.

Housing Affordability Index

DR Horton, a serious U.S. builder, reported slowing gross sales in Q3 and sees very sluggish gross sales development forward (2.8% in 2024). We expect even that is optimistic. Horton is now providing smaller houses at decrease costs.

We’ve seen gross sales collapse within the present house area (pending gross sales down -13% yr over yr), and mortgage purposes are actually at three-decade lows. With homeownership out of attain for many, one would suppose that landlords would be capable to increase rents. Not so! There was a glut of latest product, and there’s weak demand as a lot of the inhabitants that wished to maneuver throughout the pandemic have achieved so by now. In line with FNMA, emptiness charges have reached 6.5%; the 15-year common is 5.8%. And the downward strain on rents seems to be like it’s going to proceed because the file variety of condominium items beneath building are accomplished.

House Record Nationwide Hire Index and Emptiness Price

Inflation

The present inflation has fallen on the quickest tempo within the post-WWII period. Even the Manheim used car worth index, the poster little one for this specific inflation pandemic, has now turned unfavorable on a yr over yr foundation (-4.0%).

Value Adjustments for Selective Market Lessons

Wage development has not changed into the much-feared wage-price spiral the Fed was so fearful about. In line with Rosenberg Analysis, the three-month annualized price of wage development of +3.2% is greater than according to a 2% or decrease price of inflation, as productiveness confirmed up as +4.7% in Q3 and +2.2% Y/Y. Quoting Chairman Powell (his November 1 press convention):

The wage will increase have actually come down considerably over the course of the final 18 months to a stage the place they’re considerably nearer to that stage that might be according to 2% inflation over time.

The NY Fed’s International Provide Chain Stress Index (The “Bottleneck Index”) was -1.74 customary deviations under its common in October. That is the bottom studying on file.

Customary Deviations from Common Worth

We even have world meals costs off -10.9% from a yr in the past and down -25% from its peak.

UN Meals and Agriculture World Meals Value

The Baltic Dry Index is now down -74% from its October 2021 peak. And the world’s largest container shipper, Moller-Maersk, simply introduced a -10,000 individual layoff! It wasn’t that way back, when the price of delivery a container, if they might even be discovered, was $20,000+.

As mentioned in previous blogs, China is already in Recession. Their Producer Value Index has been falling for a number of months as have the costs of their exports. As identified by Economist David Rosenberg, that signifies that China is exporting deflation.

Export Value Index – China

To cap off the dialogue of inflation, the expansion of the Cash Provide (M2) is now, for the primary time in historical past, unfavorable. For monetarists, which means deflation is simply across the nook!

M2 YoY% Change

The Fed’s personal inside views are that inflation is quickly falling. The NY Feds inflation gauge is at a 30-month low and on a steep decline, whereas the San Francisco Fed predicts that inflation shall be nil by the tip of 2024.

NY Fed Underlying Inflation Gauge & SF Fed Inflation Forecast

Ultimate Ideas

- The underlying employment knowledge are signaling weak spot. Our view is that the unemployment price shall be rising for the following a number of quarters.

- We additionally imagine that the NBER will mark the beginning of the Recession on this quarter, This autumn.

- The danger of deflation is actual. A light Recession will pull inflation down towards 0%; but when the Recession isn’t so delicate, we may have a bout of deflation.

(Joshua Barone and Eugene Hoover contributed to this weblog)

[ad_2]

Source link