[ad_1]

All in all, stock for properties in good situation at acceptable sale costs stays low. Value … [+]

Through the second quarter of 2023, New York Metropolis’s actual property market has been as unstable as our inventory market. Whereas the marketplace for ultra-luxury flats, each apartment and co-op, has remained sluggish, the smaller items, which have been having a run in April and far of Might, have now sunk into the doldrums as properly. Within the one and two-bedroom market, properties which may have commanded a number of bids in April have now sat unpurchased by way of the month of June. On condition that financial realities have really improved a bit because the begin of the yr, the slowdown in buy exercise can most likely be attributed to variations within the notion of worth between consumers and sellers.

Days on Market | Manhattan

Some components of the market current challenges which make their lack of attraction to purchasers extra comprehensible. Poor situation stays an infinite barrier to the sale of properties throughout the value, dimension, and site spectra. With development assist troublesome to seek out, provide chain points persevering with to affect installations, and a basic backlog of labor as fewer contractors elect to work within the metropolis, each the prices and the timelines for giant renovations stretch properly past a yr. And in these co-ops which nonetheless have summer season work guidelines, the timelines, and thus the prices, stretch out virtually indefinitely. Anybody shopping for in a big co-op in a constructing with summer season work guidelines is all however assured a three-year undertaking, throughout which period the customer, along with paying for the renovation, should proceed to pay for his or her present lodging in addition to carrying the upkeep every month on the property being renovated.

The difficulty of month-to-month funds additionally slows consumers down. Lately, as all of the prewar and early postwar buildings close to or transfer past their a hundredth birthdays, the necessity for ongoing upkeep has pushed up upkeep costs, as has town’s more and more skeptical angle in direction of abating taxes. On the similar time, labor prices proceed to rise. At this level, labor and taxes comprise properly in extra of fifty% of what co-op and apartment homeowners pay every month. And lots of maintenances are at twice or two and a half occasions what they have been a decade and a half in the past, whereas apartment carrying prices, stripped as they now are of tax abatements, can simply run $15,000 or $18,000 and even $20,000 per thirty days for a pleasant 2,000-square-foot unit with good gentle. The rise in rates of interest, in fact, solely exacerbates this difficulty.

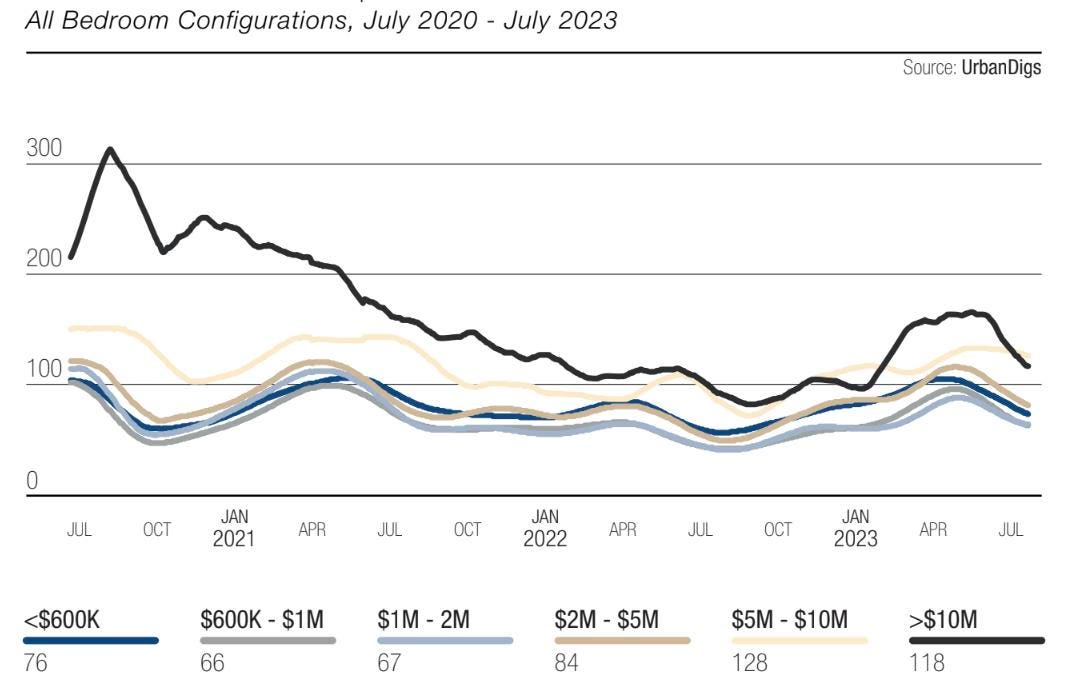

Signed Contracts | Manhattan Luxurious

On the similar time, the Olshan Luxurious Report on signed contracts for properties listed at $4 million and above exhibits a special actuality. In latest weeks, trades within the $4 million and up vary have logged their greatest numbers in years. How can these two views co-exist? Whereas I feel the explanations are complicated, I see some clues.

The overwhelming majority of gross sales in our market happen at $1.5 million and under. That is adopted by gross sales between $1.5 million and $3 million. Whereas the large gross sales (at $10 million or extra) get all of the press, they don’t drive the market. So whereas there was a rise in purchases at $4 million and above, that enhance is greater than offset by the lower in gross sales, in the course of the month of June specifically, on the decrease numbers the place the vast majority of gross sales happen. As to the better numbers reported by Donna Olshan, these replicate, greater than the rest, vendor value capitulation. Every little thing is salable when the value appropriately displays {the marketplace}. Even in Donna’s numbers, nonetheless, it’s value noting two issues: virtually no gross sales happen for $10 million or extra, and despite the fact that co-ops nonetheless outnumber condos (though not by a lot), the Olshan Report sometimes incorporates between two and three apartment gross sales for each co-op sale. This can be a reality to which co-op board members must be paying consideration!

Month-to-month Closed Gross sales | Manhattan

Ordinarily, in occasions like these, with a purchase order market through which consumers are on the lookout for better reductions than sellers are reconciled to giving, consumers could flip to leases as a short-term answer. Not really easy in 2023! Though the rental market has cooled barely over the arc of the previous three months, rents stay at their highest historic ranges in mid- and downtown Manhattan, Brooklyn, and Queens, with no signal of the wave breaking any time quickly. Very restricted provide mixed with monumental demand makes virtually each rental costing $5,000 or much less a sizzling commodity; such a spot is more likely to lease in a matter of days, typically with a number of bids.

All in all, stock for properties in good situation at acceptable sale costs stays low. Value reductions, ceaselessly not substantial sufficient to pique purchaser curiosity, move by the a whole lot by way of listings web sites each week, and 4 persons are preventing for each $4,000 rental in a lot of Manhattan, Brooklyn, and Lengthy Island Metropolis.

It seems to be like an extended sizzling summer season forward for New York actual property.

[ad_2]

Source link