[ad_1]

The Millennials have taken a lot generational bashing that it’s nearly grow to be passe. This apparently entitled bunch of the supposedly spoiled ought to have been the wreck of us all if they’d lived all the way down to their billing. How way more, then, ought to we worry the rise of Generations Y and Z? They are going to definitely lead us operating off the sting of a sluggard’s monetary cliff!

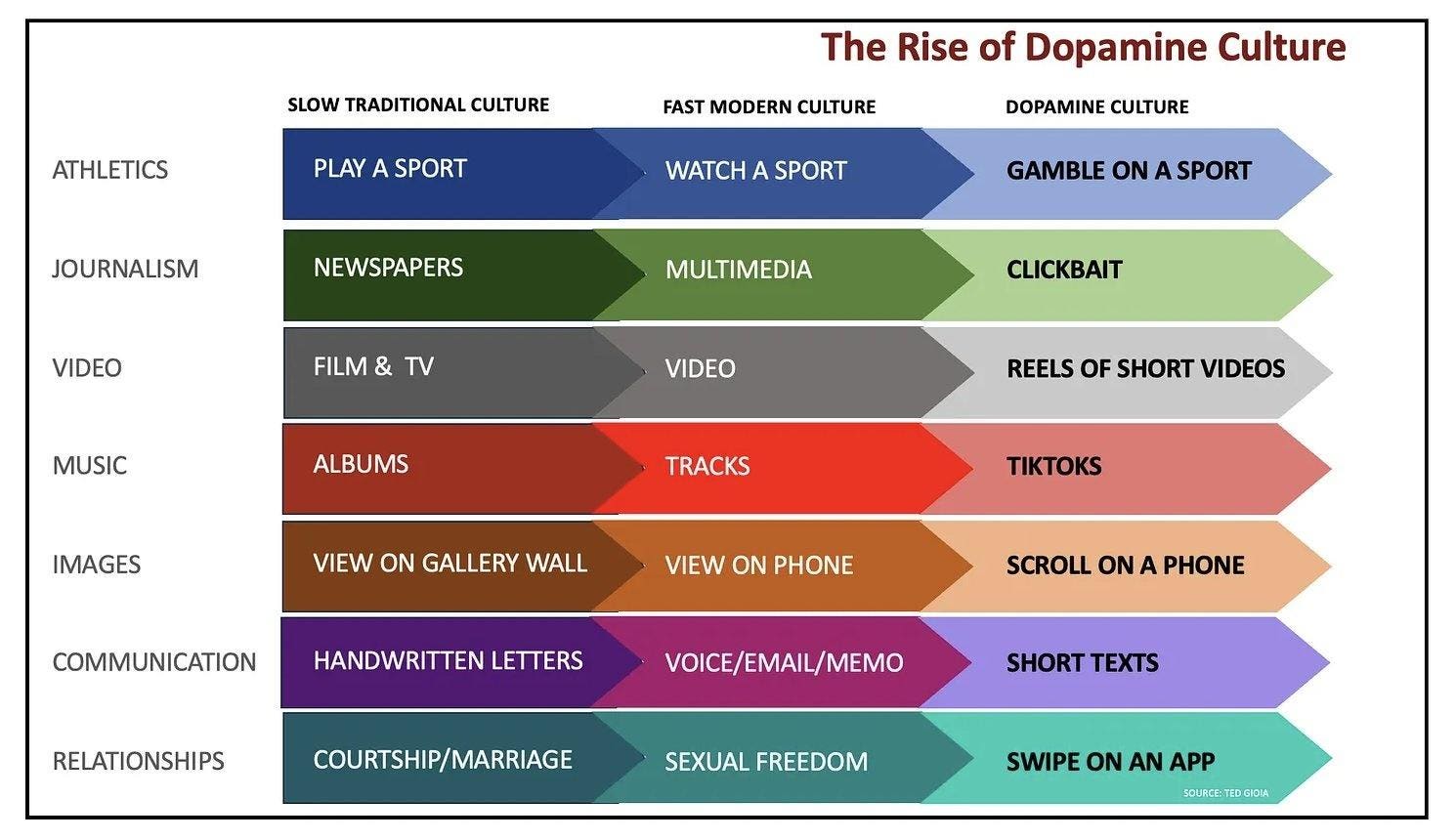

Certainly, I noticed a compelling (nevertheless curious) infographic designed to light up the autumn we’re all headed for because of the “Rise of Dopamine Tradition”:

The Rise of Dopamine Tradition

However upon nearer examination, you understand fairly shortly that that is simply good ol’ generation-shaming propaganda, hyperbolizing each the purer practices of the commentator and the worldview of the corrupted commentated. And lest we conclude that there actually is one thing uniquely damning about at present’s youthful generations, let’s recall that it is a long-standing apply.

Certainly, the generations which are most frequently celebrated at present have been criticized of their day. The homeowners of most of at present’s wealth, the Child Boomers (1946-1964), with all their peace and expression, have been the infamous antagonists of the Silent Technology (1928-1945). And people free-wheeling Flappers have been topic to the condemnation of the exterior buttoned-upness of the Best Technology (1901-1924). All of the whereas the Misplaced Technology (1883 – 1900) was criticized by older generations for his or her cynicism and lack of respect for custom.

But we neglect that usually, by the point the earlier technology is sufficiently old to gripe in regards to the current (whom they raised!?), the current has developed into the long run, bringing a number of improvements with it. Gen Z, particularly, might show to be one of the vital financially match, even from a generational perspective.

For instance, a brand new examine by the Funding Firm Institute (ICI) finds that “Gen Z households have practically thrice extra property within the [retirement] plan accounts (adjusted for inflation) that Gen X households did on the similar age.” Extra Gen Z-ers have retirement plans arrange and so they’ve saved extra in these accounts.

If you happen to have been prepared, nevertheless, to attribute this out-pacing to Gen Z’s ethical superiority—not so quick. The very fact is that a lot has improved in regards to the system, too. Outlined contribution—aka 401(okay) and 403(b) plans and the like—are way more widespread, an innovation for which the youthful generations owe the older a debt of gratitude.

However maybe essentially the most highly effective increase in retirement financial savings comes from the sphere of behavioral economics and finance. Thanks particularly to behavioral economics OG’s, Richard Thaler and Cass Sunstein’s, perception, 401(okay) plans now have extra foresight:

- Plans are opt-out as an alternative of opt-in. That manner as an alternative of getting to consciously resolve if you wish to cede a significant portion of your wage at present to your future self, the default setting for many employers is automated enrollment.

- Plans have auto-escalation choices. It’s also possible to resolve simply as soon as to extend your contribution mechanically yearly—an advance that got here from the behavioral perception that it’s simpler for us to pledge cash within the current that we received’t truly make investments till the long run.

- Plans even have fewer funding choices—as a result of we discovered that when choices have been too plentiful, savers fell prey to evaluation paralysis.

In brief, retirement plans are extra plentiful and they’re higher designed at present, due to earlier generations, and the present generations are profiting from these developments. So maybe we are able to set the household feud apart for a technology a day and credit score each of them. All of them.

[ad_2]

Source link